What are the differences between Pillars 3a and 3b?

Pillar 3a or 3b – or both? We explain what private pension planning under Pillars 3a and 3b entails, what the key differences are, and how you can use both effectively to plan for your retirement.

Anyone saving for retirement in Switzerland will sooner or later need to consider private pension provision and the difference between Pillars 3a and 3b. The answer is not clear-cut and often lies in a combination of both forms. While Pillar 3a offers comprehensive tax advantages, Pillar 3b offers a high degree of flexibility due to the freely selectable timing of payment. A well-thought-out pension strategy makes it possible to guarantee the necessary financial security and flexibility in your retirement provision.

What is the third pillar?

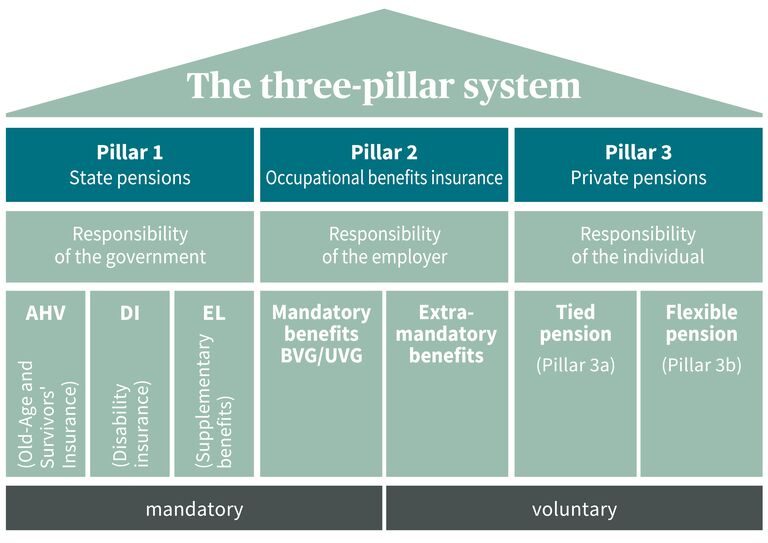

In Switzerland, Pillar 3 is private retirement provision that allows you to save for retirement in addition to state and occupational pension provision. The Swiss pension system is based on three pillars.

- Pillar 1 – OASI/InvIA/LEC– provides basic coverage in old age, in the event of disability, or in the event of death, and is mandatory.

- Pillar 2 – occupational benefits – supplements this basic insurance with mandatory pension assets paid by employers.

- Pillar 3 – private pension – is voluntary and can be paid in as either tied (3a) or flexible (3b) pension provision.

As a rule, Pillars 1 and 2 only cover about 60% of your pre-retirement salary. For most people in Switzerland, this is not enough to maintain their accustomed standard of living.

This is where Pillar 3 comes in. It offers comprehensive options for systematically closing pension gaps and building up the necessary financial stability for old age. Pillar 3 also helps you build up pension coverage against the risk of disability or death – an aspect that is particularly relevant for families and the self-employed.

What is Pillar 3a and why is it tax-advantaged?

Pillar 3a means long-term, tax-optimized retirement provision.

Tied because a Pillar 3a payout at the earliest five years before you reach the OASI reference age (formerly: This means that your Pillar 3a assets will be tied up until you retire, with the following exceptions:

- Purchase of owner-occupied residential property

- Permanent emigration from Switzerland

- Becoming self-employed

- Disability or death

In such cases, Pillar 3a assets can be withdrawn. Important to note: When funds are paid from a Pillar 3a account, a one-time tax is levied, which increases progressively with the amount withdrawn. That’s why it’s a good idea to stagger your Pillar 3a payments over several years.

Pillar 3a is tax-optimized because the amount paid in can be fully deducted from taxable income. Depending on the canton and level of income, this could mean tax savings of several hundred to over a thousand francs a year.

Pillar 3a maximum amount: How much you can contribute in 2026

The statutory maximum contribution for Pillar 3a varies from year to year. For 2026, this means:

- Gainfully employed persons with a pension fund can pay in a maximum of CHF 7,258

- Gainfully employed persons without a pension fund can pay in up to 20% of their net income, up to a maximum of CHF 36,288.

- For 2025 and all subsequent years, retroactive purchases into Pillar 3a will be possible as soon as the maximum amount for the current year has been contributed in full.

What is Pillar 3b and what advantages does it offer?

Pillar 3b is the counterpart of private pension provision in Pillar 3a and comprises all assets not included in Pillar 3a – such as cash, bank account balances, real estate, securities, precious metals, and works of art.

Unlike Pillar 3a, there is no statutory requirement on annual maximum amounts under Pillar 3b: You can pay in whenever you like and withdraw your saved capital at any time. Although the deposits cannot be deducted from taxes, they can be paid out tax-free in certain cases.

Pillar 3b is particularly suited to savings goals that are not geared exclusively to retirement. This could involve, for example, financing expensive studies or building up assets in the medium term.

What are the exact differences between Pillars 3a and 3b?

The differences between Pillars 3a and 3b relate mainly to taxes, flexibility, availability and contribution limits.

Differences between Pillars 3a and 3b

| Pillar 3a – tied pension provision | Pillar 3b – flexible pension provision | |

| Purpose | Saving for retirement | According to your wishes |

| Flexibility | Premium breaks and additional or retroactive contributions possible | No premium breaks or additional contributions possible – only premium adjustments |

| Contributions are tax-deductible | Yes, fully | No, only in certain exceptional cases |

| Maximum amount for contributions | Employees: CHF 7,258 (as of 2026) Self-employed persons: CHF 36,288 (as of 2026) |

No maximum amount |

| Availability | From the OASI reference age | At any time |

| Early payment | Home ownership, self-employment, disability, death, emigration | No restrictions |

| Taxation of payment | Lump sum tax | Usually normal taxation, tax-free to some extent |

| Taxation of income | No income tax on dividends, interest, equity performance | Insurance: No income tax on dividends, interest, equity performance Banks: Dividends and interest are subject to income tax |

| Wealth tax during the term | No wealth tax – does not count as an asset | Wealth tax – counts as an asset |

Which is better – Pillar 3a or 3b?

There’s no exact answer to this question because Pillars 3a and 3b have many differences. Which is more suitable for you personally depends largely on your current life situation and your needs.

Pillar 3a is suitable if

- You want to save on taxes today

- Your primary goal is to provide for your retirement

- You want to save over the long term and see the blocking period as an advantage

- You want an insured component (disability, death)

Pillar 3b is suitable if

- You want to access capital in the short or medium term

- You have already exhausted the maximum Pillar 3a amount

- Pursue a specific medium-term objective (owning your own home, education, setting up a business)

- You want more flexibility in the choice of products (funds, ETFs, insurance)

Our tip: Regardless of your current life situation, it is advisable to first make contributions systematically up to the maximum amount into Pillar 3a. The tax deduction is the most direct and reliable way to boost your returns on retirement savings. Only then is it worthwhile to make payments into Pillar 3b.

How can I save on taxes with Pillar 3?

There are differences in tax advantages between Pillars 3a and 3b. Pillar 3a is a very powerful tool for saving on taxes:

- Deposits are fully deducted from taxable income, which reduces your taxable income every year

- Pillar 3a assets are not subject to wealth or income tax

- Although the lump sum tax will be levied on the payout, this is well below the regular income tax rate.

- If you have several 3a accounts, you can stagger the payouts, keep your lump sum tax low thanks to progression and thus save on taxes.

Although Pillar 3b offers no options for saving on taxes when you make contributions, it does when the amounts are paid out. For a Pillar 3b payment to be tax-free, the following conditions must be met:

- Pension solutions with a term of at least five years

- Conclusion of the solution before the age of 66

- Payment of Pillar 3b after the age of 60

How can I best combine Pillars 3a and 3b?

Aligning the Pillars 3a and 3b pension strategies is the best way to achieve this. For example, if you pay the statutory maximum amount into Pillar 3a every year, this will reduce your taxable income and hence your tax burden. You can then use the freed-up capital in line with your wishes and goals. Find the pension strategy that’s right for you and seek the advice of experts early on to optimally set up your private pension provision for the future.

Frequently asked questions about the difference between Pillars 3a and 3b?

Can I pay into 3a and 3b at the same time?

Yes. Payments into Pillars 3a and 3b can be made in parallel and ideally complement each other as part of a comprehensive pension strategy.

Can I have several Pillar 3a accounts at the same time?

Yes. Several Pillar 3a accounts are permitted, provided the maximum total annual contribution is not exceeded. They enable staggered payments and tax optimization in old age.

When can I start withdrawing money from Pillar 3?

You may withdraw Pillar 3a assets at the earliest five years before you reach OASI retirement age, provided you are still gainfully employed at that time. Early withdraw is possible with exceptions such as home ownership, self-employment, disability, death, or emigration. You can withdraw your Pillar 3b assets at any time.

Written by:

Nadine Graf

Nadine Graf is a theme manager and writes texts for AXA on topics related to insurance and beyond.