Pillar 1

State pension provisionTogether with the supplementary benefits under loss-of-income insurance (SB), Swiss old-age, survivors' and disability insurance (OASI/DI) forms Pillar 1 of the three-pillar model which is enshrined in Switzerland’s constitution.

The purpose of Pillar 1 is to provide financial security for the livelihood of retirement pensioners, disabled persons and surviving dependants. In Switzerland, state pension provision can only partially secure livelihood. For this reason, the supplementary benefits were introduced in 1966 in addition to the OASI/DI which was established in 1948. Since then, these two components have formed Pillar 1 of our social system.

What is the structure of Pillar 1?

Pillar 1 is divided into two parts: OASI/DI (old-age, survivors' and disability insurance), and supplementary benefits under loss-of-income insurance (SB). Pillar 1 also includes earnings compensation during military service (LEC) and for maternity, as well as unemployment insurance.

OASI/DI and supplementary benefits (SB) differ mainly as regards the way they are financed. OASI/DI is financed by a pay-as-you-go method based on the principle of solidarity. For this purpose, pensions in progress and other benefits disbursed are paid for by the salary contributions of the working population. On the other hand, supplementary benefits are funded directly from Federal and cantonal tax. The following graphic gives you more information about the structure of Pillar 1.

Old-Age and Survivors' Insurance (OASI)

Old-Age and Survivors' Insurance is Switzerland’s mandatory state pension insurance. It secures a person’s financial livelihood in old age, and pays surviving dependants' pensions to widows and widowers following a death.

Contribution obligation

As a general rule, all employed persons domiciled in Switzerland must pay OASI contributions. Contributions are deducted from the salary by the employer, and are used directly to pay for pensions currently in progress, according to the pay-as-you-go principle. Employers and employees pay equal shares of the amounts to be transferred. The obligation to make contributions to OPA begins when you turn 17 and ends when you (both men and women) reach the reference age (formerly: normal retirement age) of 65.

Contribution period and contribution gaps

Each missing contribution year results in a reduction of the pension payable to the insured person in old age. This makes it important to close pension gaps of this sort within 5 years at most. The full contribution period lasts for 44 years with a reference age (formerly: normal retirement age) of 65 for both men and women. Beneficiaries can pay contribution gaps back into the OASI fund within the five-year period after such gaps arise. Alternatively, of course, they can opt for voluntary private pension provision, for example by paying into a Pillar 3a or 3b account to provide security in old age.

Personal entitlement to a pension

Entitlement to a pension from Pillar 1 is calculated on the basis of the person's individual account (IC). This account is used to calculate and record the personal income earned by an individual. Single persons receive an individual pension that, by law, must not be more than double the minimum retirement/disability pension per year. The amount of an OASI pension for married couples is calculated as half the total of both their incomes. If the total pension disbursed is 150% above the maximum pension permitted by law, the individual pensions are reduced. This fact is often forgotten when planning retirement provision, and it can indirectly lead to dangerous loss of income in old age.

Education and care credits

Anyone looking after children below the age of 16 during the period of their life when they must pay contributions will benefit from additional education credits. These are offset against the relevant annual income for the OASI pension, and they result in higher annual OASI disbursements provided that the maximum retirement/disability pension is not exceeded. Care credits can also be claimed in the same way, for example in connection with looking after relatives in need of care.

Income splitting

Income splitting means that the incomes earned by two marriage partners during the years of the marriage are split into equal portions. For this purpose, 50% of each of the two incomes is credited to the other partner’s OASI account. This regulation, introduced in 1997, applies to married and divorced couples, widows and widowers.

Retirement date

Regular retirement for both men and women is age 65. There are special provisions regarding the reference age for women who were born between 1961 and 1963 (transitional age group).

Insured persons have flexible options for withdrawing their OASI pension. Retirees can draw a monthly pension between the ages of 63 and 70, while women in the transitional age group can start drawing a pension at age 62. Early retirement leads to reductions in the pension disbursed, whereas deferral is rewarded with a higher pension. Applications must be submitted both for taking early retirement and for deferring a pension.

Benefits at retirement age

Depending on the average income earned and the resultant OASI deductions, the normal full pension is at least CHF 1,260 and at most CHF 2,520 (as at 2026). If a person is simultaneously entitled to draw a widow's / widower's pension, the higher pension is paid out. If persons charged with childcare are entitled to draw a child's pension, this will also increase the OASI pension that is disbursed, as long as the total amount does not exceed the maximum retirement/disability pension per year for single persons. A maximum of one and one half times the joint retirement income of the wife and husband applies to marriage partners.

Benefits in a death case

Surviving dependants' pensions are intended to prevent financial hardship due to loss of income when a marriage partner or parent dies. Marriage partners and divorced persons are entitled to widow's / widower's pensions, but the qualifying conditions for wives differ from those for husbands and divorced persons. Survivors' Insurance has been part of the OASI (Old-Age and Survivors' Insurance) since it was introduced in 1948.

Disability insurance (DI)

Disability insurance, introduced in 1960, is an integral component of Pillar 1 of the Swiss pension system. The purpose of DI is to mitigate the economic consequences of a health-related impairment of gainful employment.

Benefits in case of disability

Persons who, for health reasons, cannot be reintegrated into the work process to an extent of at least 40% are entitled to draw benefits from disability insurance. In this regard, DI follows the "integration before pension” principle. As well as paying pensions, the DI finances various reintegration measures: these include medical, educational and vocational measures, provision of medical aids, and much more besides.

Supplementary benefits (loss-of-income insurance, SB)

Anyone who draws an OASI or DI pension but whose income does not cover their minimum living costs is entitled to supplementary benefits. Other conditions for entitlement to draw supplementary benefits include a domicile in Switzerland with actual residence in this country, and further requirements which must be met. Unlike OASI/DI benefits, which are financed by the working population on a pay-as-you-go basis, supplementary benefits are funded from Federal and cantonal taxation.

Frequently asked questions

Who is insured under Pillar 1?

As a general rule, all people working and living in Switzerland are covered by Pillar 1.

Who has to pay OASI contributions?

Every person who lives and is gainfully employed in Switzerland must pay OASI contributions. Half of the OASI contributions are funded by the employee, and half by the employer; they are shown directly on the salary statement as the social insurance deduction.

When are supplementary benefits paid out?

Supplementary benefits are paid out when the OASI pension disbursed can no longer cover the minimum cost of living. A domicile with actual residence in Switzerland is a prerequisite for the receipt of supplementary benefits.

Always there for you

Do you have any questions, or would you like a pension consultation? We are always there for you!

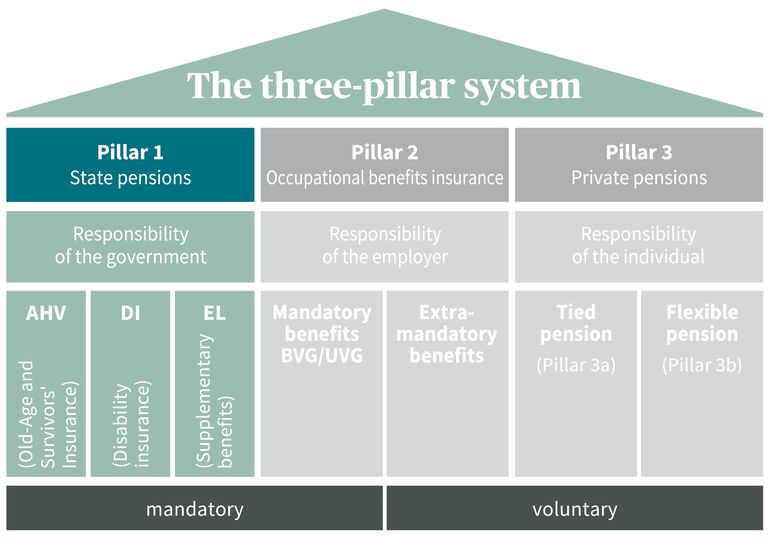

The Swiss three-pillar system

The three-pillar system: a simple explanation

The purpose of the Swiss pension system with its three pillars is to ensure financial security for people in Switzerland in old age, in the event of disability and in a death case.

Pillar 2 – occupational benefits insurance

The second pillar includes occupational benefits insurance, occupational accident insurance, daily sickness benefits insurance and the vested benefits institutions. The second pillar aims to enable people to maintain their accustomed standard of living after retirement.

Pillar 3 – private pension provision

By making voluntary payments into tied pension provision (Pillar 3a) or flexible pension provision (Pillar 3b), you can close income gaps from Pillars 1 and 2 of the Swiss social system to the fullest extent possible.