How can I protect my family?

Starting a family brings sudden changes to your life – including your financial situation: As all at once you have a lot more responsibility. How can a family protect itself against the main risks? In this guide, you’ll find out everything you need to know about insurance and provision for your loved ones.

Not long now! Whether you’re married or cohabiting, living as a patchwork or rainbow family, the arrival of a baby turns life upside down. Suddenly everything revolves around this tiny, fascinating creature. Becoming a parent is the most wonderful and overwhelming thing there is. Insurance coverage and pension provision are often forgotten in the face of sheer anticipation. But a child brings a lot of changes. Ideally, you should adjust your insurance before the baby is born – and take your time. Once your little darling arrives, you will probably have your hands full.

What happens if one parent is unavailable?

Parents want all family members to be well at all times. Dealing with worrying issues such as pension gaps or unforeseen events? Nobody likes doing that, but you have to. This is because if one parent has an accident or falls seriously ill, the family can face financial difficulties. An unforeseen loss of earnings or high additional costs can melt away the savings in your account. Some families are even forced into debt.

It’s particularly drastic if you can no longer afford the rent or mortgage on your own home. You should therefore make provision for the financial security of your family in exceptional situations. This risk coverage should be just as much a part of your pension provision as building up assets for old age. Our brochure “Clever planning for pensions and insurance” also offers initial guidance on financial planning in different phases of life.

How are you covered in the event of accident and illness?

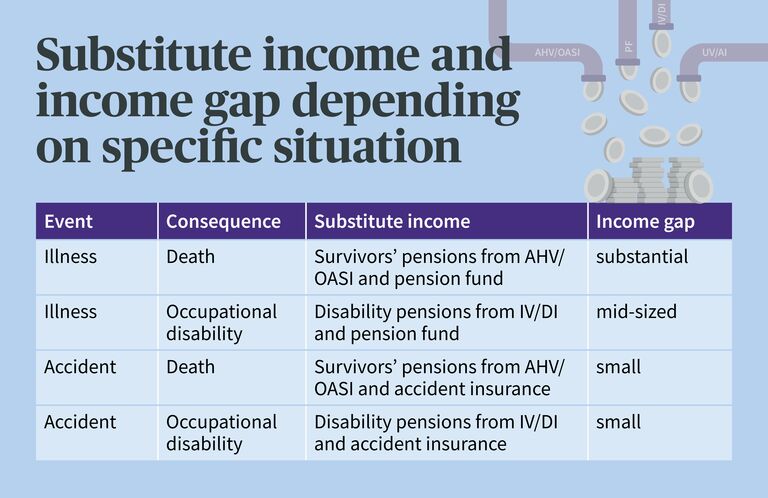

From a financial perspective, the decisive factor is what makes a person unable to work or what causes their death. Because: In terms of mandatory benefits, we in Switzerland are better insured for accidents than for illness. But the family income after such an event also depends on other factors:

- Number of children: If one parent dies or becomes unable to work, the family also receives orphan’s pensions or disabled person’s child’s pensions from the OASI or DI. The total amount paid to a family is capped (ceiling).

- Different pension fund benefits: Pension funds pay different amounts on death or disability due to illness – from the statutory minimum to generous extra-mandatory benefits (see pension fund certificate).

- Maximum salary for accident insurance: The maximum pensionable salary under accident insurance is CHF 148,200 (as at 2026). A high salary can therefore lead to an income gap.

Depending on the situation, most families now have to make do with 50 to 90% of their original salary . If the total of pensions exceeds 90% of the insured salary, accident insurance reduces its benefits commensurately and pays only a supplementary pension to the OASI/DI.

Our tip: Make sure that your employer has voluntary daily sickness benefits insurance for you. This ensures that you receive daily sickness benefits once the statutory obligation to continue making salary payments expires. Without this insurance, there is a risk of a gap in benefits lasting several months in the event of illness: The pension fund only pays after 12 months or if there is a decision from the disability insurer.

Substitute income and income gap

What risks do family models entail?

Every family is different: You need tailor-made protection. Depending on how your cohabitation is organized, there are various options for your pension provision. In summary, the following applies:

- Protection against disability and death makes sense for most families.

- By making payments into Pillar 3a or making a voluntary purchase into the pension fund , you increase your retirement assets in a targeted way – and save even more on income tax.

- A will or an inheritance contract can be particularly relevant for providing for cohabiting, patchwork, and rainbow families.

Traditional family

The traditional family – a married couple with children – is still a common way of life. This model of life enjoys the greatest social insurance protection in Switzerland. All personal and property relationships of the married partners are regulated by law. For example, from the birth of a child, parents automatically have joint custody . They build up their pension provision together and have a mutual obligation to provide assistance as well as a mutual inheritance entitlement.

Cohabitation arrangement with children

For unmarried cohabiting couples, the law does not provide any binding rules . Any obligations between the life partners must be drawn up independently and set out in a written cohabitation agreement. Cohabiting couples are at a disadvantage if unexpected events occur: If one person dies, the survivor is not entitled to a widow’s or widower’s pension from the OASI. In the case of occupational benefits insurance, the pension fund regulations determine whether funds are earmarked for the cohabiting partner. In voluntary private pension provision, on the other hand, the beneficiaries can be freely chosen.

Single-parent family or single parents

After a separation, divorce, or death , one parent usually takes over the upbringing of the children. The financial situation varies from case to case – the single-parent family may receive maintenance payments (e.g. alimony) or pensions (e.g. for widows, widowers, and orphans). Nevertheless, many single parents are affected by pension gaps: Working is usually only possible on a part-time basis. And the budget is generally too tight to pay voluntary contributions into Pillar 3 .

Patchwork family

Every patchwork arrangement has its own history – and this often results in a complex legal situation. Parents and children are partly biologically related, partly not. Then there are also financial obligations from previous relationships. Patchwork families provide better protection through marriage and mutual stepchild adoption. Only then do inheritance and pension entitlements arise in the event of disability or death of the non-biological parent.

Rainbow family

In a rainbow family, at least one parent identifies as lesbian, gay, bisexual, trans*, or queer. In recent years, the legal protection of rainbow families has been strengthened in Switzerland: Stepchild adoption has been possible for same-sex couples since 2018, and marriage has been open to all couples since July 2022. Same-sex parents now have full parental rights, whether married or not. Nevertheless, inheritance law and social insurance are still geared towards married couples or registered partnerships. That’s why marriage and stepchild adoption are also a way for rainbow families to better secure themselves legally and financially.

Which work models require specific protection?

Not only the family model, but also the employment situation of the parents influences how well families are protected. Depending on your work model, different points need to be borne in mind.

Part-time work

Most mothers, but also more and more fathers, now work part-time, regardless of their marital status. They benefit from greater flexibility while at the same time taking on financial risks: If their health is affected by accident or illness, they receive significantly lower pensions than full-time employees. It is therefore advisable to insure against such risks as well. Part-time employees are also worse off when it comes to pension provision, so capital accumulation in Pillar 3 is very important.

Self-employment

The self-employed enjoy a great deal of freedom when it comes to their insurance – and a correspondingly high level of responsibility. Since neither Pillar 2 (pension fund) nor protection of their salary after an accident is obligatory for them, a large part of the protection is left to the entrepreneurs themselves. If individual pension provision is neglected, only a modest OASI or DI pension is left if unexpected events occur. A Pillar 3a solution and individual risk protection can help.

No or marginal employment

People who do not work at all or who work less than eight hours a week are not insured against non-occupational accidents. They must therefore insure themselves against non-occupational accidents under their mandatory health insurance (only medical expenses, not including loss of earnings). As soon as they work for an employer in Switzerland for at least eight hours a week, they are fully insured under the AIA (including loss of earnings) and can have their accident coverage canceled with their health insurer.

Incapacity for work and occupational disability?

Incapacity for work or occupational disability refers to the previous employment relationship or profession. A change of job or retraining can help. However, if there is occupational disability or incapacity for work, the injured party can no longer fully provide for themselves, regardless of their work. They are therefore wholly or partly dependent on a disability pension.

How can family members be financially supported?

In the event of occupational disability

Occupational disability insurance as a private pension guarantees your family a fixed additional income – in addition to the pensions from Pillars 1 and 2. This occupational disability pension protects the self-employed, in particular, against major loss of earnings. But employees also benefit, especially if they own residential property and want to protect their mortgage.

In the event of death

Survivors are entitled to pensions from Pillars 1 and 2 of pension provision. OASI and pension fund pensions are designed to prevent affected families from falling into financial hardship. There are three types of survivors’ pensions:

- Widow’s pensions

- Widower’s pensions

- Orphan’s pensions

Different conditions and notification obligations apply within individual social insurance schemes, especially in occupational benefits insurance, in order to justify a claim. Find out more from the occupational benefits fund regulations for your pension fund.

Term life insurance can give your family financial security. It’s also affordable for families on a tight budget – and is especially important in this case. In the event of death, the insured capital is paid out immediately, regardless of any inheritance proceedings. This way, your family will be protected against financial bottlenecks in a difficult time.

Frequently asked questions

What's the right way to protect my spouse in the event of my death?

If you die, your spouse receives benefits from Pillars 1 and 2. However, this is often less than the actual income you need – especially if you have joint financial obligations. You can fill this pension gap using preventive measures such as taking out life insurance or term life insurance.

How is my cohabiting partner protected in the event of death?

Unmarried couples have no mutual legal entitlement to inherit if one partner dies. Individual pension solutions such as a cohabitation agreement or a will ensure that the life partner can inherit. It is also advisable to register your partner with your pension fund and to designate them as a beneficiary in your Pillar 3a and 3b savings plans.

What’s the right way to protect my children in the event of my death?

If the children are still minors or still in education, the OASI pays an orphan’s pension if you die. In addition, in a legally valid will, you can distribute your estate and stipulate the guardianship rules in line with your wishes. A rule on how the inherited assets are to be managed should also be included in a will.

Who inherits my savings when I die?

That depends on your marital status. If you are married or live in a registered partnership, the savings are distributed to your children and spouse according to the legal line of succession or the marriage contract. If you are unmarried, any biological or adopted children receive the lion’s share – the next heirs in accordance with the legal order of succession are your parents, siblings, and their children. An unmarried life partner must be explicitly designated in an individual pension provision plan, otherwise they will end up empty-handed. If you leave a will, the persons listed in the will will be taken into account.

What’s the difference between incapacity for work and occupational disability?

Incapacity for work refers to the previous employment relationship or profession. A change of job or retraining can help. However, if there is occupational disability or incapacity for work, the injured party can no longer fully provide for themselves, regardless of their work. They are therefore wholly or partly dependent on a disability pension.

Written by:

Anina Sabourdy

Anina Sabourdy is an Online Editor at AXA. She researches and writes on various insurance topics and loves the versatility of her job.