Pillar 3: An investment strategy for families and a way of providing for your old age

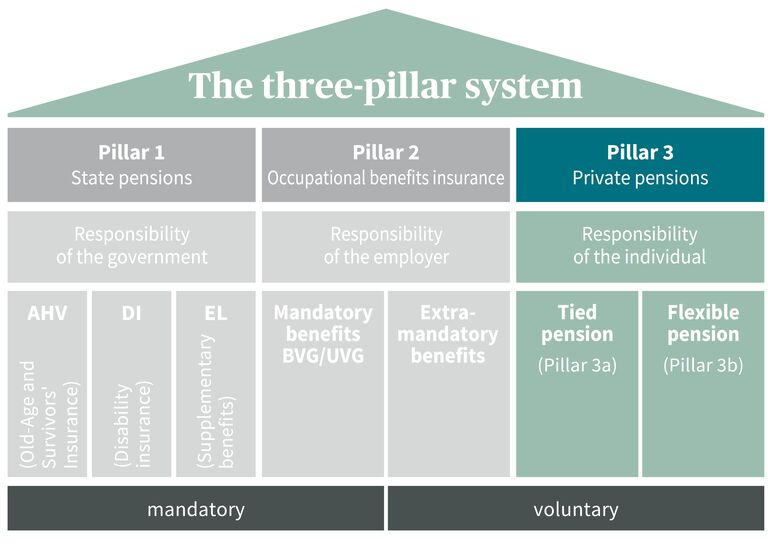

Pillar 3 enables you to make private provision for your old age. Designed to be used alongside the OASI state pension (Pillar 1) and occupational pension schemes (Pillar 2), it is also a popular means of financing home ownership. Pillar 3 is a way of encouraging individuals to save for their old age. What does private pension provision consist of? Pillar 3 can be subdivided into Pillars 3a and 3b:

- Pillar 3a: This is tied private pension provision for the self-employed and salaried employees. Contributions paid into Pillar 3a schemes can be deducted from taxable income. They are tied; i.e. they are not freely accessible at all times. Up to 20% of an individual's annual earnings can be paid in, subject to a maximum of CHF 7,258.

- Pillar 3b: This is flexible, non-tied pension provision for all. There is no limit to the amount of contributions that can be paid in. Tax deductibility is less generous than for Pillar 3a savings.

Tax deductibility: How can Pillar 3a help my family save?

Pillar 3a private pension provision works as follows: First, you pay in a predefined contribution. You can then deduct your Pillar 3a contributions from your taxable income for purposes of direct federal, cantonal, and municipal taxes. You can easily reduce your tax bill by several hundred francs, depending on how much you earn and where you live.

What is the maximum amount I can pay into Pillar 3a?

The answer will differ depending on whether you are a salaried employee or self-employed and whether or not you are in a pension scheme. The maximum contributions are as follows:

- If the individual making the contributions is a member of a Pillar 2 pension scheme: CHF 7,258 per year

- If the individual is not a member of a pension scheme: CHF 36,288 (or up to 20% of annual earnings)

The Federal Social Insurance Office sets the precise amounts that can be contributed to private pension provision on an annual basis. The annual contribution must be credited to the pension account by the end of each year.

Can funds paid into a Pillar 3a scheme be withdrawn again?

The following also applies to the relevant parent who is making contributions: Pillar 3a savings are withdrawn in full at the time of retirement, or at the earliest, five years before reaching the reference age (formerly: normal retirement age). Early withdrawals are only possible in exceptional cases under the following circumstances:

- If you wish to purchase or build your own home

- If you are leaving Switzerland permanently

- If you are taking up self-employment

- If you are switching from one self-employed activity to a different self-employed activity

- If you become 100% disabled

Do I have to pay tax when my 3a funds are paid out?

If you withdraw your Pillar 3a capital, a flat-rate tax charge will be applied separately from your other income and at a significantly lower rate. You should nevertheless bear in mind that the tax on your capital payout will increase progressively with the amount of capital. It may therefore even make sense to invest in multiple 3a solutions to enable you to spread the payout over several years.

What requirements need to be met to enable payments to be made into a Pillar 3a scheme as a family?

Anyone who is gainfully employed – including career starters and apprentices – can make private provision for their old age and pay into a Pillar 3a scheme. Payments into a Pillar 3 solution can start at any time during the current calendar year in consultation with the relevant pension fund.