The smart solution for predictable income SmartFlex income plan

New: Investment theme “Dividends”

Arrange an appointment: 052 269 21 67

Under SmartFlex, AXA invests the return-oriented component (return-oriented capital) in broadly diversified equity funds. As a customer, you have the option of choosing an investment that matches your personal convictions. You can choose between “Sustainability,” “Switzerland,” “Future trends,” ”Global,” and “Dividends.”

Regardless of the investment theme, AXA excludes sectors such as tobacco and controversial weapons and does not invest in companies that are heavily involved in coal (e.g. >10% coal in their energy mix).

Since the “Dividends” investment theme was introduced in 2026, no performance figures are currently available. Detailed performance data for the other investment themes can be found in the fund list.

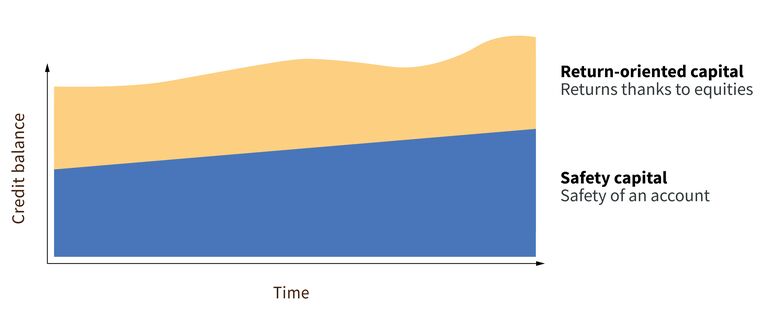

With your personal investment split, you decide how your deposit is divided: Part of it goes into interest-bearing safety capital. The other part is invested as return-oriented capital – with the chance of higher returns, but also the risk of value fluctuations. You have the option of reallocating your capital during the term of the contract.

Chart: SmartFlex premium split

Would you like to actively manage your investment risk? Take advantage of our flexible safety options, which you can customize at any time to suit your needs. Exception: Investment management can only be activated at the start. All safety options can be selected independently of each other.

As an insurance company, AXA can invest funds tied to customer contracts on a long-term basis: Pension products often have terms of several decades. This predictability makes it possible to offer attractive interest rates while maintaining a high level of security.

The SmartFlex income plan offers advantages in terms of predictability, interest rates, and security, complemented by optional safety features (free of charge).

SmartFlex vs. bank:

SmartFlex vs. pension fund:

Depending on your situation, other advantages may of course outweigh these, such as a guaranteed pension for life (pension fund) or the ability to withdraw your capital quickly and easily (bank). But be careful: Depending on interest rate increases, early withdrawal can lead to losses.

Yes, you can participate with a one-time deposit of CHF 15,000 or more. The contract term is 10 to 30 years, with the option of early termination.

With SmartFlex, you benefit from comprehensive deposit protection. In the event of bankruptcy, deposits held as safety capital are 100% protected by law. By way of comparison: Bank deposits are subject to an upper limit of CHF 100,000 per customer – any amount above this is not protected.

Deposits in return-oriented capital would also not be affected by bankruptcy. They are legally protected up to the current market value of the shares.

Do you have questions about Pillar 3 or would you like a no-obligation pension consultation? Our experts are there for you.

Families have plenty of expenses. With Pillar 3, you can easily save money and protect your loved ones at the same time.

When choosing a suitable provider for a pension solution based on Pillar 3a, interested parties are quickly faced with the question of whether to choose a bank or an insurance company.

At first glance, your pension fund certificate may seem like an incomprehensible jumble of technical terms and numbers. But when you know what you’re looking at, it’s actually pretty straightforward.