You are using an outdated browser. There may be optical and technical problems.

OK, CLOSE

Healthcare costs in Switzerland are continually rising, which is also driving up health insurance contributions. But how can you save on health insurance premiums?

There are several options, such as choosing the right insurance model, making use of government premium subsidies, and switching health insurer regularly. In this blog, we show you tips and tricks on how to make the best use of your savings potential and save on health insurance.

In addition to the standard model with a free choice of doctor, the Swiss healthcare system offers other basic insurance models. Here are three of the most common:

There are also other models with other points of contact, such as app-based offers. By choosing the right model, you can make significant savings on your health insurance premiums.

Please note: Make sure in advance that the model you want actually meets your needs. Where is your first point of contact? Do you have a free choice of doctors or does the treatment take place at an HMO practice? Is the model available in your region? Does your general practitioner belong to the insurer’s network of doctors?

The choice of excess (or “franchise”) has a direct impact on your health insurance premium. A higher excess means lower premiums, but you pay a greater proportion of your healthcare costs yourself. The opposite is true for a lower excess.

If you are healthy, rarely go to a doctor, and have financial reserves, the highest excess (usually CHF 2,500) is advisable. Otherwise, it makes more sense to stick with the lowest option (CHF 300). The intermediate levels are usually not worthwhile.

Some health insurers offer a family discount under certain conditions. For example, if you insure two children with them. Check with your provider to see if you can save on health insurance premiums this way.

If your health insurance doesn’t offer a family discount, it’s worth comparing premiums for different ages with various providers. By registering your children with a cheaper health insurance fund, you can save hundreds of francs on premiums.

Use our neutral health insurance comparison to find the right basic insurance for you in just a few clicks.

If you are financially able to do so, you can save on health insurance premiums by paying them semi-annually or annually instead of monthly. Some insurance companies reward this with a discount of up to 2 percent.

The average monthly premium for basic insurance in 2024 was CHF 359.50.

Another way to save money with your health insurer is to make use of a premium subsidy. In Switzerland, almost 30 percent of those insured – especially children, young adults, and the elderly – are eligible.

Cantonal rules determine who can benefit from such a subsidy. Each canton determines independently who is entitled to a premium subsidy, how much the reduction amounts to, and what the procedure is. Some cantons pay a premium subsidy automatically, while others require an application. You should therefore check whether you meet the requirements and contact your municipal authority if in doubt.

If you are an employee who works at least eight hours per week, you are automatically insured against accidents under the AIA (in German). Accident coverage is therefore not necessary under your basic insurance. By excluding this, you can save up to 10 percent on your health insurance premiums.

Private accident insurance makes sense to supplement the benefits provided by compulsory AIA accident insurance. Private insurance offers more comprehensive benefits than accident insurance from the health insurer and does not require an additional excess or deductible.

The easiest and quickest way to save on health insurance is to split basic and supplementary insurance – this means that you do not take both of these out with the same provider. This way, you can find the best offers that are right for you and benefit from low premiums.

Note: Unlike with basic insurance, the insurer is under no obligation to accept you for private supplementary insurance. Your application may therefore be rejected based on your state of health. For this reason, never terminate an existing supplementary insurance policy until the new insurer has confirmed acceptance in writing.

Under certain circumstances, such as during military service, it is possible to suspend health insurance or reclaim the contributions paid towards it. Check with your health insurance fund, especially as regards application deadlines.

Probably the most valuable tip for saving on health insurance premiums is to compare the different health insurers each year. This is because the benefits under basic insurance are defined by law and are the same for all providers. By contrast, the premiums can vary considerably from one health insurer to another.

Use our neutral and independent health insurance comparison to see at a glance what the premiums are for the various insurers.

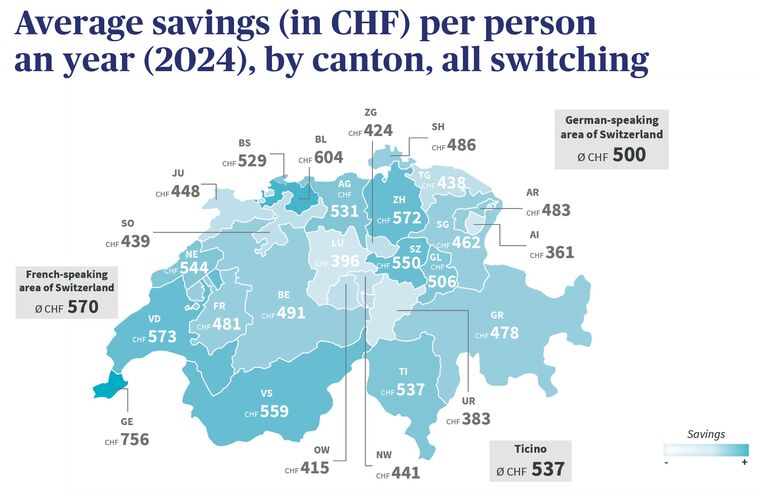

Depending on the household and policy, you can save several hundred francs a year on health insurance premiums by systematically switching. In 2024, AXA customers reduced their basic insurance premiums by a total of 23 million francs by taking out cheaper basic insurance (see AXA switching report). So it’s worth comparing premiums regularly and identifying the health insurer with the best rate. Another thing to note is the differences in savings by canton:

Please note: The savings only come about when AXA Healthcare customers switch their basic insurance and not, for example, when they take out supplementary insurance with AXA.

Nadine Graf is a theme manager and writes texts for AXA on topics related to insurance and beyond.