AXA Foundation for Occupational Benefits Conversion rate and retirement pensions

Find out the most important facts about the conversion rate and how your future pension will be calculated.

When you retire, you must decide how you would like to withdraw your accumulated retirement assets from the pension fund. You have three options:

The amount of your future retirement pension depends, among other things, on the amount of retirement savings you have accumulated and the conversion rate.

As a rule of thumb: Retirement assets x conversion rate = annual pension.

At the AXA Foundation for Occupational Benefits, the conversion rate for women and men retiring at the age of 65 is 5.2%.

The conversion rate depends on the retirement age. In the event of early or deferred retirement, the conversion rate is lower or higher. The conversion rates according to retirement age can be found in the conversion rate table.

In the pension portal on myAXA, you can view your retirement assets at any time, calculate your expected retirement pension, and simulate early or partial retirement.

Insureds with extra-mandatory retirement assets of at least 30% will be able to adapt the amount of retirement and partner’s pensions in line with their individual circumstances. You can increase your retirement pension – in which case the insured partner’s pension is lower in the event of your death. Conversely, you can increase the partner’s pension in the event of death – in which case your own retirement pension will be commensurately lower. You can specify your preferred option when you register for retirement. You don’t need to take any action until then. Find out more: Options for your retirement and partner’s pension.

The Foundation has amended the conversion rate model as of January 1, 2025. Since January 1, 2025, a comprehensive conversion rate of 5.2% has applied to all men and women at age 65. For everyone born in 1964 or earlier who was already insured with the Foundation on December 31, 2024, there is a transitional solution.

The retirement assets of the transitional age category accumulated up to the end of 2024 will be converted into the future pension at the conversion rates applicable until the end of 2024 when you retire. The conversion rate of 5.2% is only applied for retirement assets that are saved from January 1, 2025.

Instead of a lifetime monthly pension, you can also opt for a lump-sum payment. With a full lump-sum payment, you will receive your entire pension fund balance as a one-time payout upon retirement. The conversion rate is then irrelevant.

You can also opt for a hybrid form, i.e. a combination of a pension and lump-sum payment. This option lets you draw part of your savings as a pension and part as a lump sum.

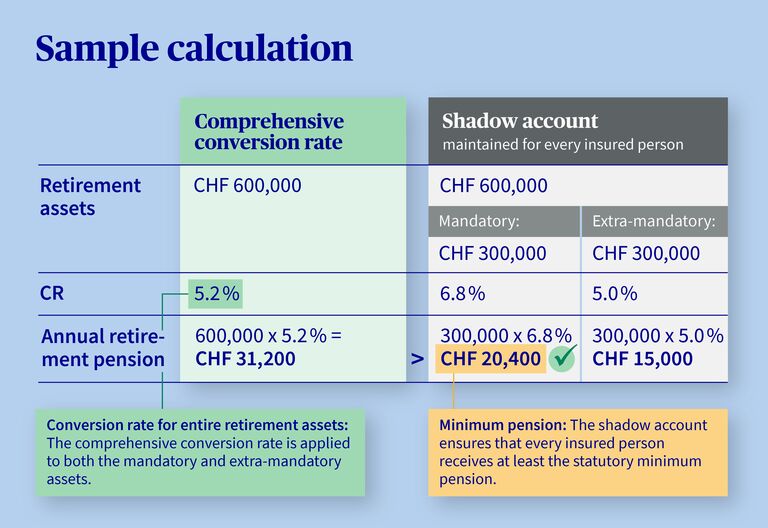

The conversion rate determines the percentage rate with which the retirement assets you have saved up are converted into an annual pension when you retire. If you have CHF 100,000 in retirement assets and the conversion rate is 5.2%, then your annual pension is CHF 5,200.

A comprehensive conversion rate means that a single conversion rate is applied to a person's entire retirement assets (i.e. both mandatory and extra-mandatory assets).

With a split conversion rate model, the mandatory and extra-mandatory portions are considered separately. A separate conversion rate is used for each portion. You can find out more about the pension fund conversion rate in the blog post.

The statutory minimum conversion rate of 6.8% applies only to the mandatory portion of occupational benefits insurance (OPA minimum) and is set by the Federal Council. In the case of the extra-mandatory portion, the pension fund sets the conversion rate itself.

Pension funds can also set a “comprehensive” conversion rate that applies to both parts together (i.e. mandatory and extra-mandatory).

Even with a comprehensive conversion rate of less than 6.8%, it is guaranteed at all times that the minimum benefits prescribed by law will be met, i.e. that the total retirement pension will be at least as high as the mandatory credit balance x the OPA minimum conversion rate. To monitor this, a control account (known as a shadow account) is kept for every single insured person.

With OASI (Pillar 1), you can start drawing a pension at the earliest at age 63.

With the pension fund (Pillar 2), you can retire at the earliest at age 58.

If you are interested in early retirement, you can find out more in the blog post Early retirement: How to retire early.

Ordinary retirement according to the OASI reference age:

If you retire at the ordinary retirement age (OASI reference age) with the pension fund, you or your employer do not need to notify the pension fund separately: The pension fund will contact you.

Around five months before you reach the OASI reference age, you will receive a letter announcing your upcoming retirement. This letter will include a calculation of your retirement benefits, additional information about retirement, and a link to an online form that you can use to tell us how you would like to receive your benefits.

Retirement before the OASI reference age (early retirement):

If you are considering early retirement, you can simulate your future pension and run through various scenarios at any time on myAXA. If you definitely wish to take early retirement, your employer must notify us of your withdrawal from the pension fund.

Retirement after the OASI reference age (up to a maximum of 70):

If you wish to continue working after the normal retirement age and already receive retirement benefits from the pension fund, you can indicate this using the online form that you will receive with the notification letter regarding your retirement.

If you wish to continue working and do not wish to leave the pension fund, but would like to defer or continue your insurance, you can also indicate this using the online form.

You only have to decide on the form of payment – i.e. pension, lump sum, or hybrid form – when you retire.

Ideally, you should already start thinking about your retirement a few years in advance. This will allow you to prepare optimally and make the right decision for you. Find out more under “Planning for retirement”.

One major advantage is the high level of security: You receive a fixed amount every month, which is paid out for the rest of your life. In the event of death, benefits for your surviving dependants are also covered, for example a partner or orphan’s pension.

One disadvantage may be that you cannot freely dispose of your entire saved assets.

With a full lump-sum payment, you will receive your entire pension fund balance as a one-time payout. You are free to decide how you would like to use your pension fund money. However, you are also responsible for investing your assets.

If you withdraw all of your capital, you will no longer have any further claims on your pension fund. Therefore, in the event of death, no partner or orphan’s pension will be paid to your surviving dependants from the pension fund.

If you have made voluntary purchases into the pension fund in the last three years before retirement, you cannot withdraw money from the pension fund in the form of capital during a three-year blocking period.

The withdrawal of capital is treated differently under tax law depending on the canton. Please check with the relevant tax office to find out how this is regulated in your canton.

The pensions portal on myAXA lets you view your retirement assets at any time and learn more about your retirement provision. You can also find your pension fund certificate in the portal under “Documents.” Furthermore, it is possible to calculate your estimated retirement pension and simulate early or partial retirement.